More than half of the 20 largest workplace pension funds grew substantially more than the industry average over five years, according to the latest Corporate Adviser Pensions Average (CAPA) data.

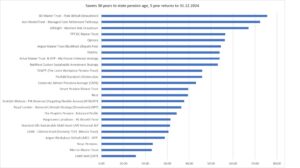

Figures for the year to Q4, 2024, showed that the SEI Master Trust – Flexi default (drawdown) delivered the highest five-year cumulative returns for younger savers. Employees with 30 years left until they reach state pension age (SPA) saw their pot increase by 75.53 percent over the period (after average charges of 0.5 percent have been applied).

This is a much higher return than the industry average, which CAPA data revealed was 43.1 percent for the same age group over the same cumulative period.

The Aon MasterTrust and LifeSight pension funds also achieved substantially higher than average five-year cumulative returns for younger savers, with 72.34 percent and 67.07 percent respectively.

What £10k turns into over 5 years

For savers, the level of return from different funds can differ significantly with even a slight increase in percentage growth. For example, £10,000 in the SEI Master Trust fund would have grown to £17,553 over five years.

A saver with £10,000 in the Aon MasterTrust account would have accumulated £17,233, while someone with the same amount in the LifeSight pension would have built up £16,706 in the same five years.

In stark contrast, the average CAPA fund would have grown to £14,310 for the same period. (See below for the full list of cumulative return percentages over 5 years for workplace pensions).

Small differences are significant

The data highlights the power of compound returns, particularly over long periods. Even a 1 percent increase in pension performance can have a big impact on an employee’s retirement pot.

The difference is clear if you compare two pension funds that start with the same amount but one grows at 5 percent annually, while the other grows at 6 percent annually.

If they both start with £10,000, over 40 years the fund that grew at 5 percent a year will reach £70,400. However, the fund with 6 percent annual growth will achieve £102,857.

In this example, the fund that grew just 1 percent more a year over 40 years has accumulated an extra £32,457 in that time.

Pension performance for retirees

For people who are about to retire (one day from SPA) a number of funds performed better than the CAPA data industry average in the year to Q4 2024.

The SEI Master Trust – Flexi default (drawdown) had the best performing one year return for savers who are one day from the SPA with 10.83 percent for the year to Q4 2024. This is a stronger return than the CAPA industry average of 7.08 percent for the same group over the same time period after average charges of 0.5 percent have been applied.

Penfold Standard Lifetime plan and Hargreaves Lansdown pension funds also performed well, growing 9.6 percent and 9.3 percent respectively for the same period.

More about this research

CAPA data is the only source of data on performance of master trust and group personal pension (GPP) default funds that is compiled from data received directly from providers. The data is not generated from calculations or projections made from third-party sources and can therefore be considered the accurate, definitive data set on DC pension defaults.

With research covering master trust and contract-based defaults with assets totalling over £500bn, together the 20 pension providers invest assets for around 17 million active and 15 million deferred UK pension savers.

For some providers, where there are separate defaults, GPP and master trust data is provided.

This is the latest data for the year up to Q4 2024 and all figures shown are after charges have been applied. For more results visit www.capa-data.com.